Landholder duty is a tax imposed on an entity when they acquire a significant interest in another entity that owns land.

The purpose of landholder duty is to ensure that entities cannot avoid paying tax on land acquisitions that are held indirectly by other unit trusts or private companies which the entity has an interest in.

When does landholder duty apply?

Landholder duty is triggered when you acquire a ‘significant interest’ in a landholding entity.

The specific thresholds and definitions of what is a ‘significant interest’ can vary depending on which state or territory you’re in, but generally, it involves acquiring a substantial percentage of shares or units in a company or trust that owns land.

The below thresholds indicate the minimum land value required for landholder duty to apply per state and territory. In Victoria, for example, the landholdings need to be worth $1 million or more for landholder duty to apply.

State/ Territory

Land value threshold

Victoria

$1,000,000

New South Wales

$2,000,000

Queensland

$2,000,000

Western Australia

$2,000,000

South Australia

No specific threshold

Tasmania

$500,000

Northern Territory

$500,000

Australian Capital Territory

Nil (i.e. applies to any interest in land

How is landholder duty calculated?

Landholder duty is determined according to the value of land owned by another entity and the percentage of interest obtained in that entity.

Each state has its own rates and thresholds, so it’s important to consult the relevant state revenue authority for specific details.

Example – Victoria

To calculate landholder duty in Victoria for acquiring a 50% interest in an entity which has a landholding valued at $2 million, follow these steps:

1.Determine the dutiable value: Multiply the value of the landholding by the percentage interest acquired.

Dutiable value = $2,000,000 × 50% Dutiable value = $1,000,000

2. Apply the relevant rate of duty: For landholdings with a dutiable value of >$960,000 to $2 million the duty rate is 5.5%.

Duty = $1,000,000 x 5.5% Duty = $55,000

Therefore, the landholder duty for acquiring a 50% interest in an entity with a landholding valued at $2 million would be $55,000.

Part II: Understanding landholder duty

To understand how landholder duty works, we need to understand the key terms in its definition.

If landholder duty applies when an entity acquires an interest in another entity with a landholding, then we need to understand what is meant by ‘landholding’, and what is classified as an ‘acquisition’.

What is a ‘landholding’?

In the context of landholder duty, a ‘landholding’ is defined fairly broadly, and refers to any interest in land owned by a company or trust. This includes:

Direct ownership of land

Interests in land, such as leasehold interests

Fixtures

Land held by a subsidiary of the landholder

Land held in trust where the landholder or its subsidiary is a beneficiary

What it doesn’t include:

Interests held by secured creditors

Estate or interest of a mortgagee

Profit a prendre

Complexities can arise in the practical applications of some of these inclusions/ exclusions, and it’s best to describe this complexity by going through an example.

Example

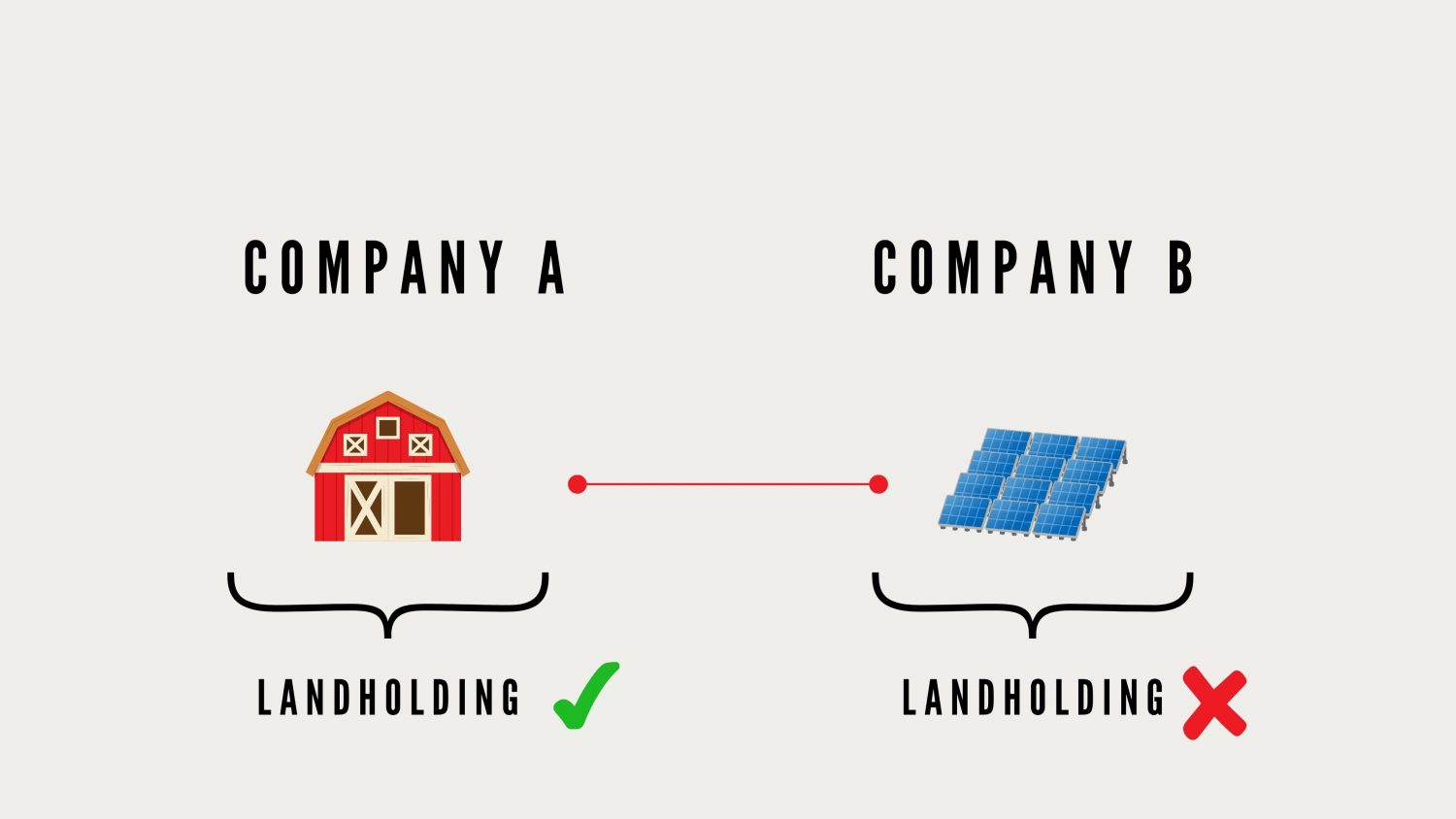

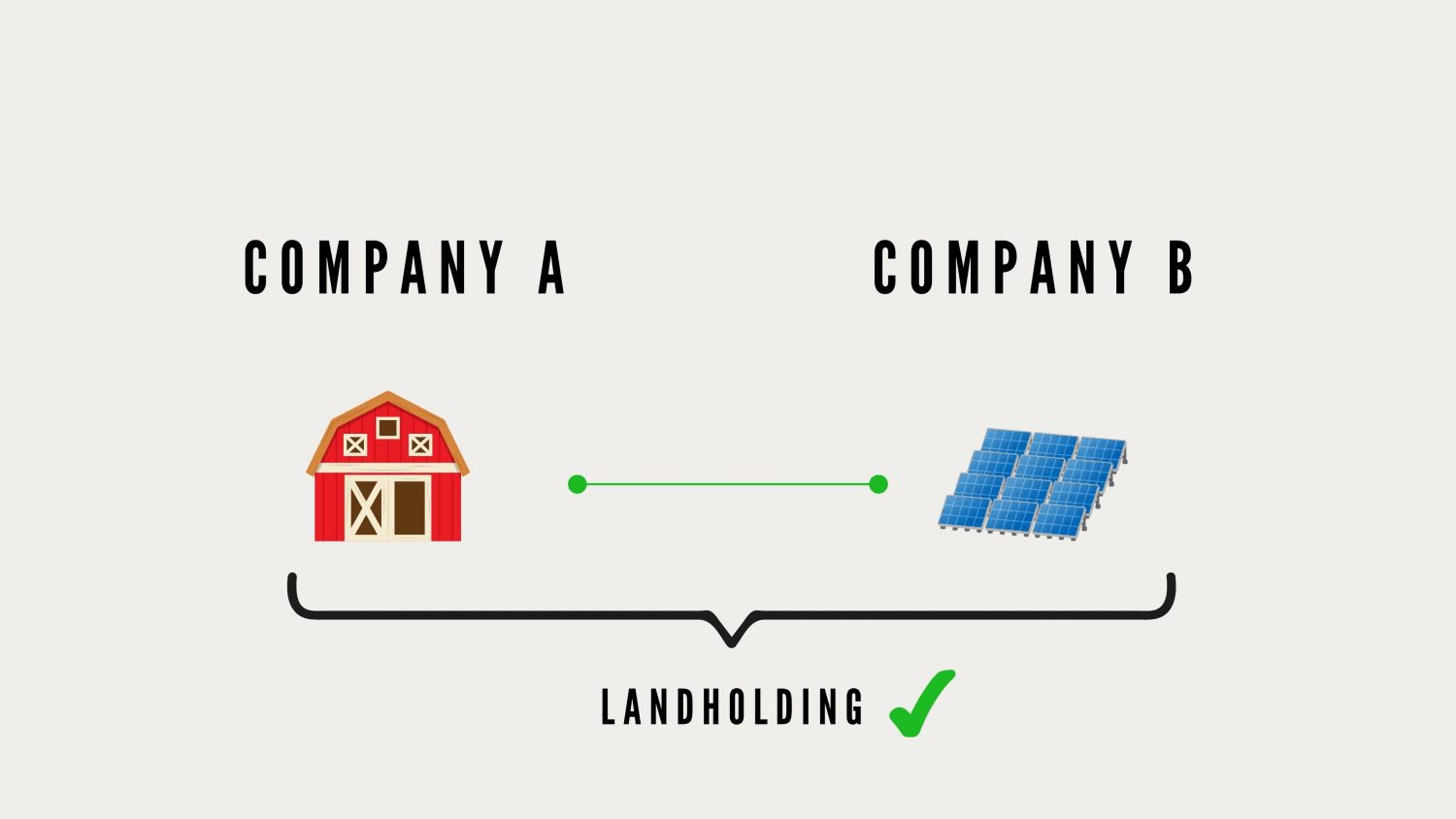

If Company A owns farmland, the land on which that farm exists is a part of Company A’s landholding.

Now, consider solar panels affixed to land on that farm.

Are solar panels, being a fixture, included in Company A’s landholding?

On the face of it, any fixture on Company A’s land is part of its landholding irrespective of who owns the fixture. As such, if those same solar panels on Company A’s land are owned by Company B, they will still ordinarily be considered as part of Company A’s landholding.

However, in the above situation, in Victoria for example, Company A can apply to the Commissioner of State Revenue to exercise their discretion to not treat the solar panels as part of its landholding on the basis that:

another entity owns them (i.e. Company B), and that entity is not associated with company A; and

the solar panels are not used by Company A in connection with the land – as such, the solar panels are not used by Company A in the operation of the farm (e.g. for electricity).

However, if the solar panels are used to generate electricity to run the farm, regardless of whether they are owned by Company A or Company B, they may still be considered as part of the landholding of Company A:

In the context of landholder duty, an ‘acquisition’ refers to obtaining a significant interest in a landholding entity. This can include:

Purchasing shares or units in a company or trust that owns land.

Increasing an existing interest in a landholding entity to a significant level.

Acquiring economic entitlements or benefits related to the landholder

A ‘significant’ interest typically means acquiring a substantial percentage of shares or units, which varies depending on the type of entity (e.g., in Victoria the threshold is 20% for private unit trusts, 50% for a private company or a wholesale unit trust scheme, and 90% for a listed company and public unit trust).

However, complexity can arise when aggregation rules apply. Broadly, these rules are designed to ensure that multiple related transactions are treated as a single acquisition for duty purposes, preventing taxpayers from separating related transactions to avoid paying landholder duty.

For example, in Victoria, there are three aggregation rules:

1. Prior acquisitions made by the same person

If you acquire an interest in an entity and subsequently acquire a further interest in that entity which combine to take you above the relevant thresholds, then landholder duty may apply.

2. Acquisitions made by associated persons

If two or more transactions are entered into by relatives, associates or related entities may be aggregated.

So, if you acquire a certain percentage of an interest in a private company, and then a related party such as your partner or child acquire a further interest, those acquisitions can be aggregated to take you above the relevant threshold for landholder duty to apply or to pay a higher landholder duty.

3.Associated transactions

The associated transactions rule can cause separate transactions to be treated as a single acquisition for duty purposes. This is designed to prevent the avoidance of duty by splitting a significant acquisition into smaller, non-dutiable transactions, and can catch taxpayers out when subsequent transfers collectively breach the rule.

There are also other considerations to take into account in determining whether landholder duty applies, such as obtaining economic interests in a landholder or in situations where you exert control over the operational decisions of a landholder entity.

In these situations, it’s best to get legal advice to clarify your options.

Part III: Challenging landholder duty

If you believe that you should not have to pay landholder duty, or that the duty is incorrect for some reason, you may look to understand whether an exemption or concession applies, or if you have grounds to dispute the duty.

What are the exemptions and concessions to landholder duty?

If you qualify for exemptions or concessions, you may attempt to challenge the duty assessment.

If an exemption applies, the acquisition of an interest in a landholder is completely free from duty under specific circumstances.

Some examples of where exemptions can apply include:

you had been transferred the land directly

acquisitions are made by registered trustees in bankruptcy

acquisitions are made by liquidators

acquisitions are made by administrators of deceased estates

there is a pro-rata increase in interests across unit holders or shareholders

If a concession applies, it will involve a reduction in the amount of duty payable rather than a complete exemption.

A common example of a concession applies in situations where an unfair or unintended duty outcome would occur, such as if the duty exceeds what would be payable for a direct transfer of the land. In such cases, the Commissioner of State Revenue has the discretion to reduce the duty payable.

How to get an exemption or concession for landholder duty?

In advance of acquiring interests in another entity, you can apply for a private ruling from the relevant revenue authority on the application of the landholder duty to your prospective acquisition.

If you are in the process of being investigated, you can put forward your reasons to the relevant revenue authority as to why an exemption would apply.

If landholder duty has already been assessed, then you can consider lodging an objection to claim the exemption.

How do I dispute landholder duty?

As a taxpayer, you may consider challenging landholder duty under several circumstances:

1. Incorrect assessment: If you believe the Commissioner of State Revenue has made an error in calculating the duty, such as misvaluing the land or duty rate, or incorrectly determining the percentage of interest acquired, you may have grounds to challenge the assessment.

2.Aggregation issues: If you believe that one of the aggregation rules has been applied to acquisitions incorrectly such that an inflated duty liability is imposed, you may have grounds to dispute the aggregation. For example, you may have evidence to suggest that certain transactions have been wrongly considered to be associated.

3.Dispute over ‘significant’ interest: If there is a disagreement about whether your acquisition constitutes a significant interest, you may choose to challenge the duty. This can involve disputing the interpretation of thresholds or the nature of your interest in the landholding entity.

4. Capital raising transactions: If your acquisition is part of a capital raising effort and you believe it should not be subject to landholder duty, you may choose to challenge the assessment. This is particularly relevant if the transactions are structured in a way that should not trigger duty.

Challenging landholder duty can be complex, so it’s important to gather all relevant evidence and seek legal advice to follow the formal objection and appeal processes.

Understanding landholder duty is crucial for anyone involved in property transactions or investments. By familiarising yourself with the basics, including what constitutes a landholding, significant interest thresholds, and potential exemptions and concessions, you can navigate the complexities of landholder duty more effectively.

For advice on challenging your landholder duty assessment, contact Aptum.